What’s up with industrial leasing?

Welcome to another edition of The Private Investor, your monthly newsletter that provides insider access to private real estate’s latest trends, brightest minds, and top investment ideas.

This newsletter is a 4-minute read.

The Latest

To state the obvious, industrial leasing has slowed. And in some corners of the market, leasing basically ground to a halt over the past year. Yes, it’s true the industrial sector has been faring much better than other property types. After all, 2023 was yet another year of double-digit national rent growth. But the asset class certainly hasn’t been immune to macroeconomic headwinds.

Why has leasing slowed? And is it time for investors to panic? Not quite – here’s why.

What happened?

On the back of e-commerce, industrial leasing experienced unimpeded growth for over a decade, and reached a crescendo during the pandemic. The recent annual leasing totals from a new CBRE report1 are pretty astounding:

2019: 560 million SF; 2020: 720M SF; 2021: 1 billion SF

Woah, that escalated quickly. After a then-record year in 2019, leasing activity nearly doubled only two short years later. This dynamic, of course, encouraged developers to build a record number of new buildings. However, demand still overwhelmed new supply, and national vacancy rates continued to hover around a remarkably low 3%.

Now, let’s fast forward. In 2022, leasing “dropped” to 865 million SF before declining further to 790 million SF in 2023. How come? Because tenants became cautious about making major capital investments, such as opening new logistics facilities, while faced with rising financing costs and economic uncertainties, per Green Street2. Weaker demand was especially pronounced among big box users. Industrial sector pros have been calling the trend of recent lower leasing levels “a return to normal” relative pre-pandemic years.

The issue though is while leasing has cooled, supply has not.

Another 156.3 million SF of industrial facilities were completed in Q4 2023. That’s the second highest quarterly total on record (only behind the 173.2 million SF delivered in the previous quarter), according to Cushman & Wakefield3. While tenants can wake up one morning and decide they want to hold off on making a lease decision, developers don’t have this luxury. They need to finish what they started, which is why new projects that broke ground in the first half of 2023 are still being delivered, even though tenant demand has paused.

This has caused the national vacancy rate to creep up to 5.2%, up from the boom-market lows but still below the 10-year pre-pandemic historical average.

What happens next?

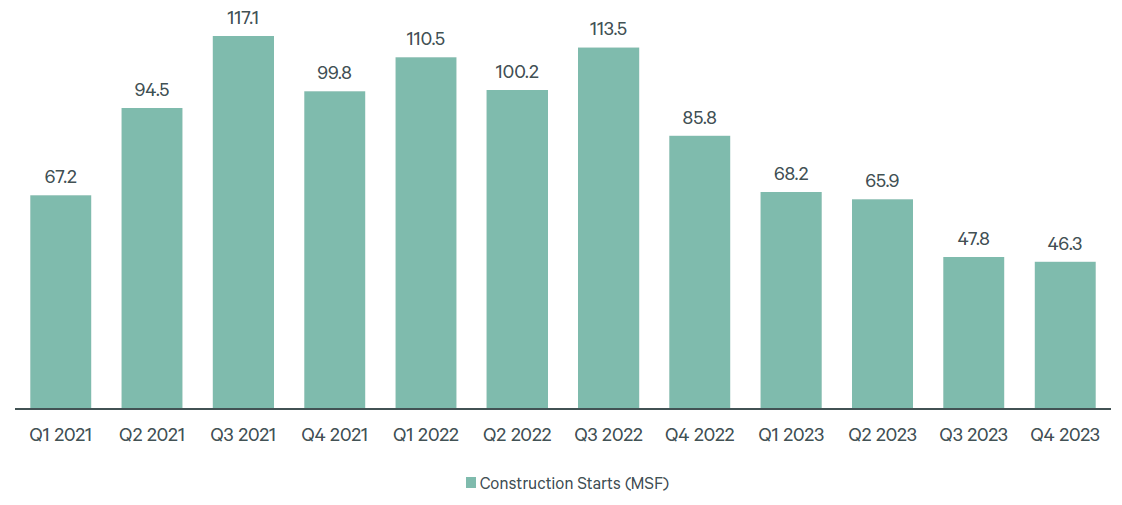

The market needs to digest more new supply over the first half of 2024. That means vacancy rates will likely tick higher. However, in the second half of the year, new deliveries will drop off a cliff. CBRE points out new construction starts have declined for five straight quarters due to market uncertainty and a difficult lending environment.

Source: CBRE Research Q4 2023

As for tenant demand, macroeconomics will determine what happens next. If inflation continues to stay low, the Fed cuts interest rates, and consumer demand stays strong, then tenants are expected to jump off the sidelines. If inflation ends up being sticky, interest rates stay high, and consumer demand weakens, then it could be another slow year for industrial leasing activity.

In 2025 and beyond though, Cushman & Wakefield and CBRE both agree most Tier 1 industrial markets are expected to be undersupplied. The historical growth engines for the sector still remain – ecommerce growth and supply chain resiliency.

CBRE says e-commerce still only accounts for 23% of non-auto or gas related retail sales and is expected to grow to 26% in the next few years and 34% in 10 years. More goods sold online will result in more demand for industrial space to deliver goods to consumers at increasingly faster speeds.

Separately, companies are embracing onshoring and nearshoring after the pandemic shined a light on significant vulnerabilities in our nation’s supply chains. Other recent supply chain issues include the Suez Canal obstruction, Russia-Ukraine War, Panama Canal drought, Houthi attacks in the Red Sea, and others.

Helping matters, the U.S. government has bolstered supply chain resiliency by pouring tens of billions of dollars into the cause through the Inflation Reduction and CHIPS acts. This will undoubtedly have significant positive upstream and downstream impacts on demand for industrial real estate.

Bottom Line

Yes, industrial leasing has been taking a temporary breather. But it’s a matter of “when”, not “if” tenants will start signing more leases at new, modern buildings. E-commerce, onshoring and nearshoring will make sure of that.

In the meantime, investment in the sector will favor a nuanced approach. Smaller assets will be attractive, plus larger deals in select, underserved markets.

CBRE: The State of the U.S. Industrial & Logistics Market - January 2024

Green Street: U.S. Industrial Outlook - January 2024

Cushman & Wakefield: Industrial Q4 2023 Marketbeat